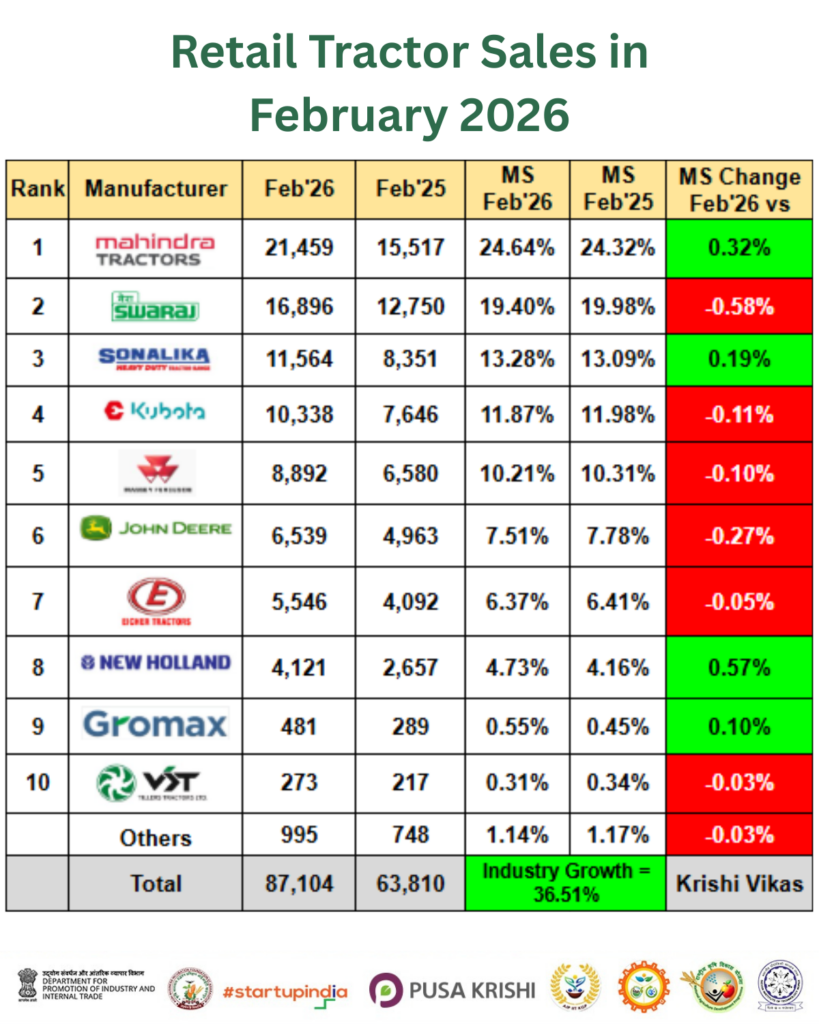

India’s retail tractor market witnessed impressive growth in February 2026, with total sales reaching 87,104 units, compared to 63,810 units in February 2025. This marks a significant 36.51% year-on-year increase, reflecting stronger rural liquidity, better crop earnings, and consistent replacement demand across major agricultural regions.

Alongside higher sales volumes, the month also saw noticeable shifts in market share among leading tractor manufacturers, highlighting increasing competition within the industry.

Retail Tractor Sales Performance – February 2026

Mahindra continued to dominate the market, selling 21,459 tractors, up from 15,517 units last year. The company strengthened its leadership position as its market share rose slightly from 24.32% to 24.64%.

Swaraj retained the second position with 16,896 units, compared to 12,750 units in February 2025. Although sales increased, its market share declined marginally from 19.98% to 19.40%, indicating growth slightly below the overall industry pace.

Sonalika recorded strong performance with 11,564 units, improving its market share from 13.09% to 13.28%, showing competitive gains during the month.

Escorts Kubota Limited sold 10,338 units, higher than last year’s 7,646 units. However, its market share dipped slightly from 11.98% to 11.87%.

Massey Ferguson reported 8,892 units, compared to 6,580 units last year. Despite solid volume growth, its market share saw a minor decline from 10.31% to 10.21%.

Together, the top five brands accounted for 69,149 units, contributing nearly 79.39% of total retail tractor sales, showing how concentrated the Indian tractor market remains among leading players.

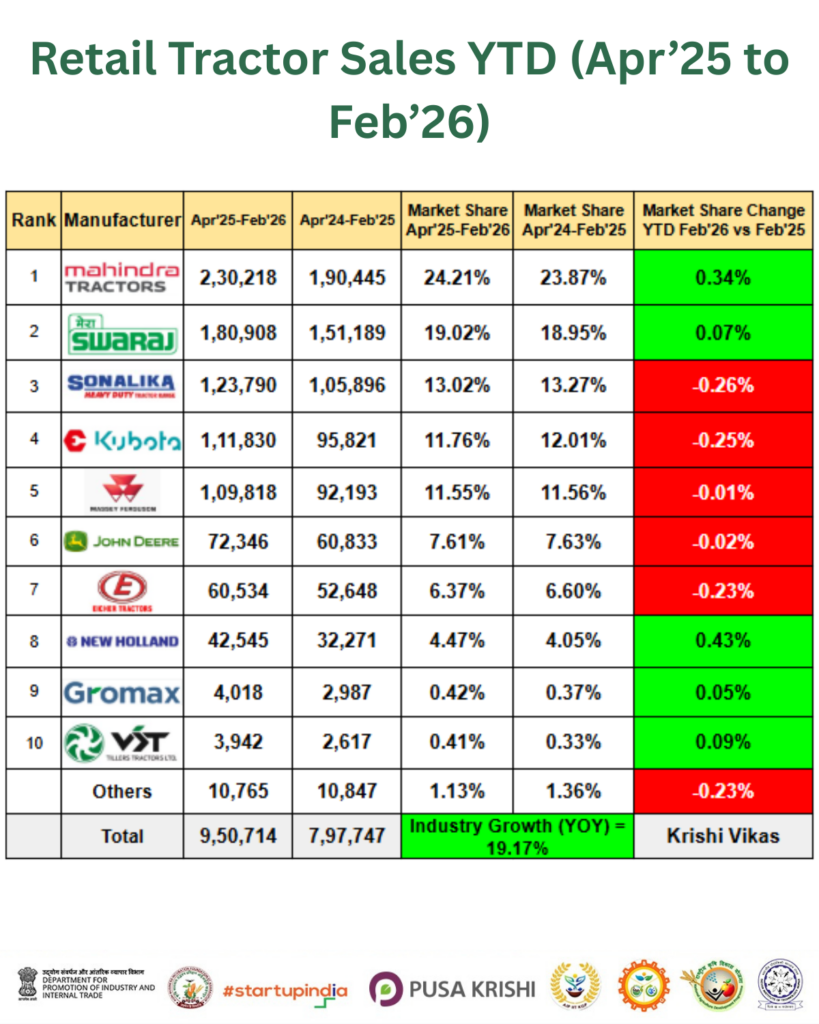

Retail Tractor Sales YTD (April 2025 – February 2026)

During the April 2025 to February 2026 period, total retail tractor sales reached 9,50,714 units, compared to 7,97,747 units during the same period last year — a strong 19.17% year-on-year growth.

- Mahindra & Mahindra led cumulative sales with 2,30,218 units, increasing its market share to 24.21%.

- Swaraj recorded 1,80,908 units, with a slight market share improvement to 19.02%.

- Sonalika sold 1,23,790 units, though its market share declined slightly to 13.02%.

- Escorts Kubota registered 1,11,830 units, with a small drop in market share to 11.76%.

- Massey Ferguson achieved 1,09,818 units, maintaining almost stable market share at 11.55%.

The top five brands together contributed 7,56,564 units, accounting for nearly 79.58% of total YTD retail tractor sales.

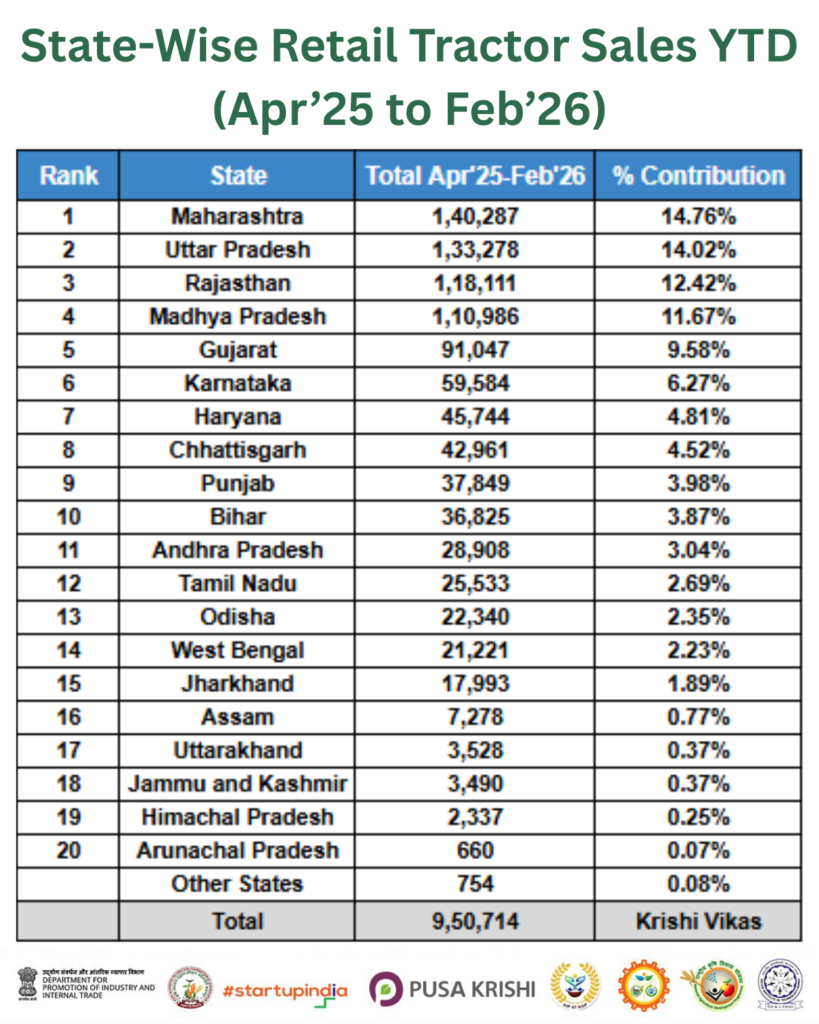

State-wise Contribution to Tractor Demand

Tractor demand continues to remain concentrated in key agricultural states:

- Maharashtra led with 1,40,287 units (14.76% share)

- Uttar Pradesh followed with 1,33,278 units (14.02%)

- Rajasthan recorded 1,18,111 units (12.42%)

- Madhya Pradesh contributed 1,10,986 units (11.67%)

- Gujarat secured fifth position with 91,047 units (9.58%)

Combined, these five states accounted for 62.45% of total retail tractor sales during the YTD period, highlighting strong regional concentration in demand.

Conclusion

The Indian tractor industry demonstrated strong momentum in February 2026, supported by improving rural conditions and positive agricultural sentiment. While most leading brands reported healthy volume growth, slight shifts in market share indicate evolving competition within the sector.

With the top brands contributing nearly 80% of sales and demand heavily driven by key agricultural states, the industry appears well-positioned to sustain growth in the coming months if favourable rural trends continue.